Business Bank Account Singapore: 7 Powerful Easy Tips

Starting a company is exciting… but the banking side? That’s where many business owners suddenly feel stuck. You register your company, build your website, maybe even land your first customer, and then you realize you still need a reliable business bank account Singapore companies actually trust.

And honestly, choosing the wrong account can quietly hurt your business for years.

Hidden fees. Slow transfers. Terrible online banking. Limited international support. Some founders don’t notice the problem until money starts moving at scale. By then, switching banks becomes frustrating and time-consuming.

Singapore has become one of the strongest business hubs in Asia. Startups, ecommerce brands, consultants, agencies, tech companies, and international entrepreneurs all want access to Singapore’s banking ecosystem. But with traditional banks, digital banking platforms, and fintech options competing for attention, choosing the right business bank account Singapore solution can feel overwhelming.

The good news? It’s simpler when you know what actually matters.

This guide breaks everything down in plain English. You’ll learn how business banking works in Singapore, what documents you need, which banks are popular in 2026, common mistakes founders make, and how to choose an account that actually supports growth instead of slowing it down.

Whether you’re a local entrepreneur, foreign founder, freelancer, ecommerce seller, or SME owner, this guide should help you make a smarter banking decision without wasting weeks researching random forums and outdated advice.

What Is a Business Bank Account Singapore?

A business bank account Singapore companies use is a financial account designed specifically for commercial transactions. Unlike a personal bank account, it separates company finances from personal money and supports operations like payroll, vendor payments, invoicing, tax filing, international transfers, and payment collection.

Sounds basic. But it matters more than many founders think.

When your business finances are mixed with personal spending, accounting becomes messy very quickly. Tax reporting gets harder. Investors lose confidence. Banks may even question transaction legitimacy if your account activity looks inconsistent. A dedicated singapore business banking account creates structure from day one.

Most corporate bank account Singapore solutions include online banking, debit cards, multi-user access, international transfers, accounting software integration, and business payment solutions. Some also offer foreign currency accounts, automated invoicing tools, expense management systems, and ecommerce integrations.

Traditional banks like DBS, OCBC, and UOB still dominate the local market. They’re trusted, stable, and packed with business features. But digital platforms are growing fast too. Fintech providers such as Wise and Airwallex are attracting startups because they offer lower fees, faster setup processes, and smoother international payments.

And here’s the interesting part…

The “best” business bank account Singapore option depends heavily on your business model. A local retail shop may prioritize cash deposit access. A remote agency may care more about international transfers. Ecommerce businesses often need payment gateway support and multi-currency accounts. Startups usually focus on low fees and speed.

This is why blindly following recommendations online can backfire.

A startup business bank account Singapore founders love may be terrible for a manufacturing company. Meanwhile, a premium corporate banking singapore package might be unnecessary for freelancers or small agencies just starting out.

The smartest move is understanding your actual business needs before comparing banks.

Why Businesses Need a Dedicated Business Account

Some small business owners initially try to operate using personal accounts. It seems easier at first. Less paperwork. Faster setup. No corporate verification process.

But that shortcut creates problems surprisingly fast.

A proper business bank account Singapore setup builds professionalism and financial credibility. Clients take your business more seriously when invoices come from a registered company account instead of a personal name. Suppliers trust you more. Payment tracking becomes easier. Even accounting software works better with structured business banking systems.

And banks notice these details too.

If you eventually apply for financing, loans, or credit facilities, your banking history matters. Financial institutions want clean records. Consistent cash flow. Organized statements. A business account creates that financial trail naturally over time.

There’s another big advantage people overlook — legal separation.

Singapore businesses, especially private limited companies, are legally separate entities from their owners. Using a singapore company bank account reinforces that separation. This becomes especially important during audits, disputes, or compliance reviews.

For startups and SMEs, modern business banking singapore services also improve efficiency. Many accounts now integrate directly with accounting platforms like Xero and QuickBooks. Some automate recurring payments and invoice reconciliation. Others allow multiple team members with permission controls.

That saves time every single month.

Foreign entrepreneurs benefit even more from structured banking. A foreigner business bank account Singapore setup can simplify international business operations, support cross-border transactions, and improve credibility when dealing with Asian suppliers or clients.

And if your company deals internationally, multi-currency support becomes critical. Many business owners lose money through poor exchange rates without realizing it. A multi currency business account Singapore solution can reduce currency conversion costs dramatically over time.

Business banking isn’t just about storing money anymore.

It’s becoming an operational tool that directly affects efficiency, reputation, scalability, and profitability.

Types of Business Bank Accounts in Singapore

Not every business account works the same way. Singapore banks and fintech companies now offer several categories depending on company size, transaction volume, and operational needs.

The most common option is the business current account singapore companies use for daily operations. These accounts support incoming payments, outgoing transfers, payroll, and vendor transactions. They usually include online banking and debit card access.

For smaller companies or startups, SME business bank account Singapore solutions are often more practical. These accounts usually offer lower minimum balances, simplified fee structures, and startup-friendly features. Some even waive fees during the first year.

Then there are digital business banking singapore platforms.

These accounts have exploded in popularity because they reduce paperwork and simplify international business operations. Digital banks and fintech providers focus heavily on user experience. Faster onboarding. Better mobile apps. Lower transfer costs. Cleaner dashboards.

They’re especially attractive for remote teams and ecommerce businesses.

Another option is the business savings account Singapore businesses use for reserve funds. These accounts typically offer higher interest rates but fewer transaction capabilities. They’re useful for storing emergency capital or tax reserves separately from operational cash flow.

International businesses often choose online corporate account Singapore solutions with multi-currency support. These accounts help businesses receive and send payments globally while avoiding excessive conversion fees.

And yes, traditional banks still matter.

DBS business bank account Singapore services remain popular because of strong local infrastructure and integration with Singapore’s business ecosystem. OCBC business account Singapore packages are widely used among SMEs. UOB business bank account Singapore solutions appeal to companies needing regional Asian banking support.

The rise of fintech banking has also created hybrid options.

Platforms like Wise and Airwallex aren’t technically banks in every sense, but they offer flexible business payment solutions singapore companies increasingly rely on. Lower FX fees, virtual cards, and faster global transfers make them attractive alternatives.

The important thing is choosing based on actual operational needs — not marketing hype.

How to Open a Business Bank Account Singapore

Opening a business bank account Singapore entrepreneurs can use legally and efficiently usually takes anywhere from a few days to several weeks depending on the bank and your company structure.

The process has become easier recently, but banks still take compliance seriously.

First, your company must usually be registered with ACRA in Singapore. Once incorporated, you’ll prepare required documents including your business registration certificate, company constitution, director identification documents, shareholder details, and proof of business activity.

Some banks may request additional information.

This could include invoices, contracts, website links, business plans, or explanations of expected transaction activity. Businesses with international shareholders or complex ownership structures may face stricter verification procedures.

That’s normal.

Singapore banks maintain strong anti-money laundering standards, and they carefully review high-risk industries or international applications.

For local founders, opening a singapore business account opening package is usually straightforward. Many banks now allow partial online applications before requiring final verification.

Foreign entrepreneurs sometimes face more challenges.

A business bank account for non residents Singapore setup may require physical presence during verification. Some banks insist directors visit a branch personally. Others allow remote onboarding under specific conditions.

This is one reason digital banking platforms are growing quickly. Fintech providers often offer much faster onboarding processes compared to traditional banks.

The actual steps generally look like this:

- Register your Singapore company

- Compare business banking providers

- Gather required documentation

- Submit your application

- Complete identity verification

- Deposit initial funds if required

- Activate online banking access

One thing many founders underestimate is preparation.

Incomplete paperwork delays applications constantly. Banks may reject applications simply because business activities aren’t clearly explained. A professional website, business email address, and organized documentation improve approval chances significantly.

And timing matters too.

If you’re planning company incorporation and bank account Singapore setup simultaneously, coordinate both processes carefully. Some corporate service providers bundle incorporation and banking assistance together to simplify onboarding.

That can save time — especially for overseas entrepreneurs.

Business Bank Account Singapore Requirements

The exact business bank account Singapore requirements vary slightly between banks, but most institutions ask for similar core documents and verification details.

At minimum, you’ll usually need:

- Company incorporation documents

- ACRA business profile

- Company constitution

- Passport or ID of directors and shareholders

- Proof of residential address

- Board resolution approving account opening

- Description of business activities

Some banks may also request:

- Contracts or invoices

- Website and social media links

- Estimated transaction volume

- Source of funds explanation

- Tax residency information

This surprises some founders at first.

They expect banking to be simple after incorporation. But Singapore banks are highly regulated, especially regarding international transactions and compliance monitoring.

If your business involves crypto, gambling, high-risk investments, or complex international structures, expect additional scrutiny.

Foreign-owned companies often face stricter onboarding procedures too. A foreigner business bank account Singapore application may involve enhanced due diligence checks. Banks want to understand who controls the company, where revenue comes from, and whether operational activities align with stated business purposes.

And yes, physical presence can still matter.

Some traditional banks require at least one director to attend an in-person verification appointment. Others have relaxed these rules depending on nationality, company structure, and risk assessment.

Digital-first providers tend to move faster.

That’s one reason singapore fintech business account solutions are attracting startups and online businesses. Faster onboarding, remote verification, and lower compliance friction appeal to modern entrepreneurs.

Still, traditional banks offer advantages too — especially for larger businesses seeking loans, merchant services, or regional banking relationships.

The best approach is preparing documentation carefully before applying anywhere. Organized applications get processed faster and create stronger first impressions with banking teams.

Costs, Fees, and Hidden Charges

Many businesses choose a bank based only on reputation. Big mistake.

The real cost of a business bank account Singapore solution goes far beyond monthly maintenance fees. Hidden charges quietly add up over time, especially for companies handling international payments or large transaction volumes.

Most banks charge a monthly account fee ranging from low-cost startup plans to premium corporate packages. Some waive these fees temporarily for newly incorporated companies. Others require maintaining a minimum account balance.

Fall below the threshold? You’ll usually pay penalties.

Transaction fees matter too.

Certain banks limit free transfers each month before charging additional costs. Cash deposit fees can apply. International wire transfers often carry both sending and receiving charges. Currency conversion spreads quietly reduce profits on overseas transactions.

And those FX margins can be brutal.

A business processing regular international payments might lose thousands yearly through weak exchange rates alone. This is why many ecommerce brands and remote businesses now use digital business banking singapore platforms with better currency conversion pricing.

Startup founders should also watch out for:

- Account opening fees

- FAST/GIRO transfer fees

- Corporate card charges

- Foreign transaction fees

- Dormancy penalties

- Multi-user access costs

- Early closure fees

Traditional banks typically provide broader infrastructure and support but may cost more overall. Fintech platforms often reduce transfer and FX expenses significantly but may lack advanced lending or local branch services.

The cheapest business bank account Singapore option isn’t always the best choice either.

Low-cost accounts sometimes limit transaction capabilities, customer support responsiveness, or integration options. A growing business may outgrow ultra-basic banking surprisingly fast.

This is where comparing real operational costs matters more than promotional marketing.

Estimate your expected monthly transfers, currencies, incoming payments, and transaction volume before choosing an account. The “best” account often depends on your actual business behavior rather than advertised pricing.

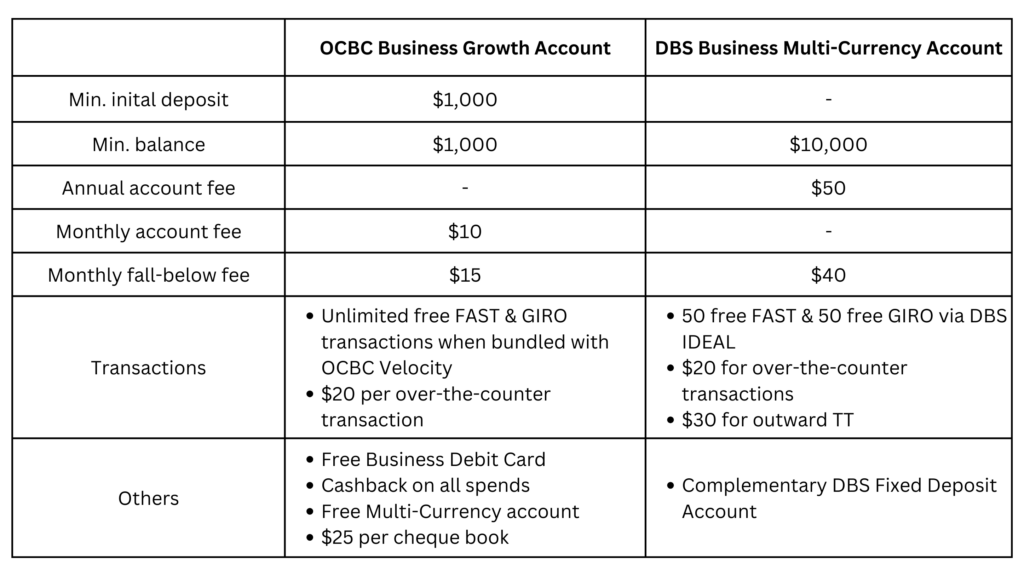

Best Banks and Platforms for Business Banking in Singapore

Singapore offers strong business banking options across traditional banks and modern fintech providers. Each serves different business types and priorities.

DBS remains one of the most recognized names for business banking services Singapore companies rely on. Their SME ecosystem is mature, online banking tools are strong, and local integrations work smoothly. Many startups choose DBS because of reliability and strong local support.

OCBC business account Singapore packages are also widely respected. OCBC performs particularly well among SMEs looking for stability and practical banking features. Their business platforms are generally user-friendly and locally focused.

UOB business bank account Singapore solutions appeal to businesses operating regionally across Asia. Companies with Southeast Asian operations often appreciate UOB’s regional presence and trade support services.

Then come the digital challengers.

Wise has become popular for international transfers and multi-currency management. Businesses handling overseas clients or suppliers often prefer Wise because of transparent exchange rates and lower conversion costs.

Airwallex focuses heavily on global commerce and startup operations. Ecommerce brands and SaaS companies often choose Airwallex for payment collection flexibility and international scaling support.

But here’s the thing…

No single provider dominates every category.

Traditional banks offer stronger credibility, financing access, and physical infrastructure. Fintech platforms provide speed, flexibility, and lower operational costs. Many businesses actually combine both strategies — maintaining a local corporate account while using fintech platforms for international payments.

That hybrid setup works surprisingly well.

When comparing providers, focus on:

- Ease of account opening

- Monthly costs

- International transfer fees

- Currency support

- Mobile banking quality

- Customer support

- Integration with accounting software

- Lending availability

- Scalability for future growth

A startup business bank account Singapore founder needs today may not fit the business two years from now. Choose a provider capable of growing with your operations.

Business Bank Account Singapore vs Personal Accounts

This comparison comes up constantly, especially among freelancers and very small startups.

Can you technically use a personal account for business transactions?

Sometimes, yes.

Should you?

Usually not.

A dedicated business bank account Singapore structure creates cleaner accounting, stronger compliance protection, and better professional credibility. Personal accounts simply aren’t designed for commercial operations.

Banks may even freeze or restrict personal accounts showing suspicious business activity patterns. Frequent incoming client payments, high transaction volume, or overseas commercial transfers can trigger compliance reviews.

And that creates unnecessary headaches.

Business accounts also provide features personal accounts don’t. Multi-user permissions, payroll systems, accounting integrations, invoicing support, corporate cards, and structured reporting tools all simplify operations significantly.

Tax preparation becomes easier too.

When personal and business expenses mix together, bookkeeping gets messy fast. Separating transactions saves accounting time and reduces reporting errors.

There’s also the legal side.

If your business operates as a private limited company, maintaining separation between company finances and personal funds reinforces corporate protection structures. Mixing funds carelessly may weaken liability protections in certain situations.

For international businesses, a proper singapore bank account for companies setup improves credibility with overseas clients and suppliers. It signals legitimacy and operational professionalism.

So yes, opening a dedicated account requires more effort initially. But long term, it usually saves time, stress, and operational complications.

Expert Tips for Choosing the Right Business Account

Choosing the right business bank account Singapore provider isn’t about picking the “most famous” bank. Smart founders think strategically about how banking affects operations, growth, and cash flow.

Start with transaction behavior.

Do you process mostly local payments? International transfers? Ecommerce sales? Subscription revenue? Different business models need different banking strengths.

If you operate globally, prioritize multi-currency support and competitive exchange rates. A multi currency business account Singapore setup can save substantial money over time.

Customer support matters more than people realize too.

Banking issues rarely happen at convenient times. Slow support during payment problems can seriously disrupt operations. Research real user experiences before committing.

And test the digital experience.

A clunky banking dashboard becomes frustrating fast when you use it daily. Smooth mobile access, quick approvals, and intuitive interfaces genuinely matter.

Another smart strategy? Think beyond current size.

Many startups choose ultra-basic accounts that become restrictive later. Switching banks during rapid growth can be painful. It’s often better to choose scalable banking solutions from the start.

Automation is another underrated factor.

Good online business bank account Singapore platforms integrate with accounting software, payroll tools, and ecommerce systems. These integrations reduce manual admin work every month.

Security matters too.

Strong fraud monitoring, two-factor authentication, and user permission controls protect your business from operational risks.

And don’t rush applications.

Some founders apply to the first bank they see online without comparing fees or requirements properly. Spend a little time researching first. The right decision can improve operations for years.

Common Mistakes to Avoid

Business owners make the same banking mistakes repeatedly.

The first is choosing based only on brand recognition. Big names don’t automatically mean the best fit. Some businesses overpay heavily for features they barely use.

Another mistake is ignoring international transfer costs.

Currency conversion fees quietly drain profits over time, especially for ecommerce brands, agencies, and import businesses. Compare actual FX spreads carefully before choosing a provider.

Many startups also underestimate future growth.

An account that works for five monthly transactions may collapse under larger operational demands later. Scalability matters.

Documentation mistakes cause delays too.

Incomplete paperwork, vague business descriptions, and inconsistent company information frequently slow down singapore business account opening applications. Professional preparation improves approval speed dramatically.

Some founders also ignore digital usability.

A slow, outdated banking interface wastes time daily. Modern businesses need efficient mobile banking and clean online workflows.

And one major mistake? Keeping all funds in one account.

Smart businesses often separate operational cash, tax reserves, payroll funds, and savings buffers across different structures. That improves financial organization and risk management.

Frequently Asked Questions

How long does it take to open a business bank account Singapore companies can use?

Traditional banks may take anywhere from several days to several weeks depending on compliance checks. Digital banking platforms often move faster and may approve accounts within days.

Can foreigners open a business bank account in Singapore?

Yes. Many banks support foreign-owned companies, although requirements can be stricter. Some banks require physical presence for verification while others allow partial remote onboarding.

Which bank is best for startups in Singapore?

It depends on your needs. DBS, OCBC, and UOB remain strong traditional choices. Wise and Airwallex are popular among startups needing international payment flexibility and lower transfer costs.

What documents are needed for a singapore company bank account?

Most banks require incorporation documents, identification for directors and shareholders, proof of address, company constitution, and business activity details.

Is a digital business banking singapore platform safe?

Reputable fintech platforms use advanced security systems and regulatory compliance measures. Still, businesses should research licensing, security features, and operational reputation carefully.

Can I open a business bank account before incorporating my company?

Usually no. Most providers require completed company registration before opening a corporate account.

Final Thoughts

Choosing the right business bank account Singapore solution is one of those decisions that seems small at first… until your business starts growing.

Then it affects everything.

Cash flow. International payments. Team operations. Accounting efficiency. Customer trust. Expansion opportunities. Even stress levels.

The good news is Singapore offers excellent banking options for nearly every type of company. Traditional banks provide strong credibility and infrastructure. Fintech platforms deliver speed and flexibility. Hybrid setups combine both advantages surprisingly well.

The key is choosing intentionally.

Don’t just follow random recommendations online. Think about how your business actually operates today — and where it’s heading tomorrow.

If you’re launching a startup, running an SME, building an ecommerce brand, or expanding internationally, now is the time to build a banking structure that supports long-term growth instead of limiting it.

Research your options carefully, compare fees realistically, prepare documentation properly, and choose a provider aligned with your business goals.

A strong business banking foundation won’t guarantee success.

But it definitely makes growth easier.

And if you’re currently exploring singapore startup banking solutions or planning company incorporation and bank account Singapore setup, consider speaking with experienced business advisors or banking specialists before making a final decision. The right guidance can save significant time and money later.

You may also like

Leave a Reply